Executive Summary

What you need to know

If 2025 has a challenge for B2B marketers, it's this: Do more with the

same. Or

less.

APAC marketers are under pressure to hit bigger pipeline goals with flat or shrinking budgets. 59% of

these

marketers have the same or less budget and more than half are putting budget into demand gen over brand.

Worryingly, just 37% believe their current budget will get them there - yet most aren't

doubling down on the areas that will truly make a difference.

This Green Hat & 6sense study of 155 APAC B2B marketers reveals a profession in tension - with investment

areas

not lining up with what marketers say they value most.

The report unpacks where APAC marketers are investing but also where they're not. And it does so through

the

lens of our APAC B2B Buyer Journey Research Report, which tells us:

- The average buying group comprises 12.8 people who will only reach out to vendors

73% through a 13 month buying journey.

- 82% choose the first vendor they engage with.

- More than half of the buying group are ‘hidden' buyers - they can influence or veto

decisions but often aren't directly targeted by marketing.

The disconnect between priority and budget allocation is real:

- Brand priority vs. budget share

Brand building ranks #1 in importance yet demand generation is still getting more budget

(and increasing

faster).

Why keep favouring short-term performance when brand drives early preference and

long-term

growth?

- AI confidence vs. budget commitment

80% of marketers are confident in AI having a positive impact on marketing goals - but only

29% have

carved out budget for it.

If AI has potential to unlock efficiency and scale, why isn't it being funded more

deliberately?

- ABM maturity gap

55% of APAC marketers run ABM programs vs. 77% in the US.

Why is a region so focused on growth lagging behind on the most fundamental form of

account-centric

marketing?

What does this mean for marketers?

Marketers are between a rock and a hard place.

Tight budgets, rising revenue targets clash with long buying cycles, and self-directed buyers

who only reach

out late in the buying cycle. In the face of this pressure, marketers report defaulting to

activities that

drive short term gains at the cost of longer-term goals.

Success in 2025-26 will come down to a marketer's ability to:

-

Align budget allocations with long buying cycles:

Even though content, brand and ABM are seen as strategic, many teams still over-index on short-term

tactics

such as lead gen - often because they're easier to measure against a backdrop of increased pipeline

demands -

even if they don't reflect how B2B decisions are made.

-

Build a brand that's front of mind with buyers:

From our research, nearly everyone in the buying group knew the winning vendor's brand before

engaging them.

Brand equity and mental availability are what get you shortlisted, especially when 82% of buyers

engage their

preferred vendor first. Brand also plays a key role in overcoming buyer indecision.

-

Get more out of Account-Based Marketing (ABM):

You're influencing a buying group of 13, many of whom you'll never meet. ABM, not demand gen, is the

only

model that matches how B2B buying decisions are really made.

-

Make AI the new competitive edge:

It's not just about which tools you use. It's how you create more content, optimise campaigns

faster, get

richer insights, and work at a pace your competitors can't match. When budgets are tight, AI can be

your

efficiency engine.

This report highlights how you can get more out of your 2025-26 budgets by aligning investments with

areas that

will drive results.

We recommend you read this report alongside the APAC B2B

Buyer Journey

Research Report that unpacks how B2B buying teams are operating in this region.

Part A

Marketing budget priorities

The illusion of stability: a story of rising revenue goals, reallocation and

misalignment.

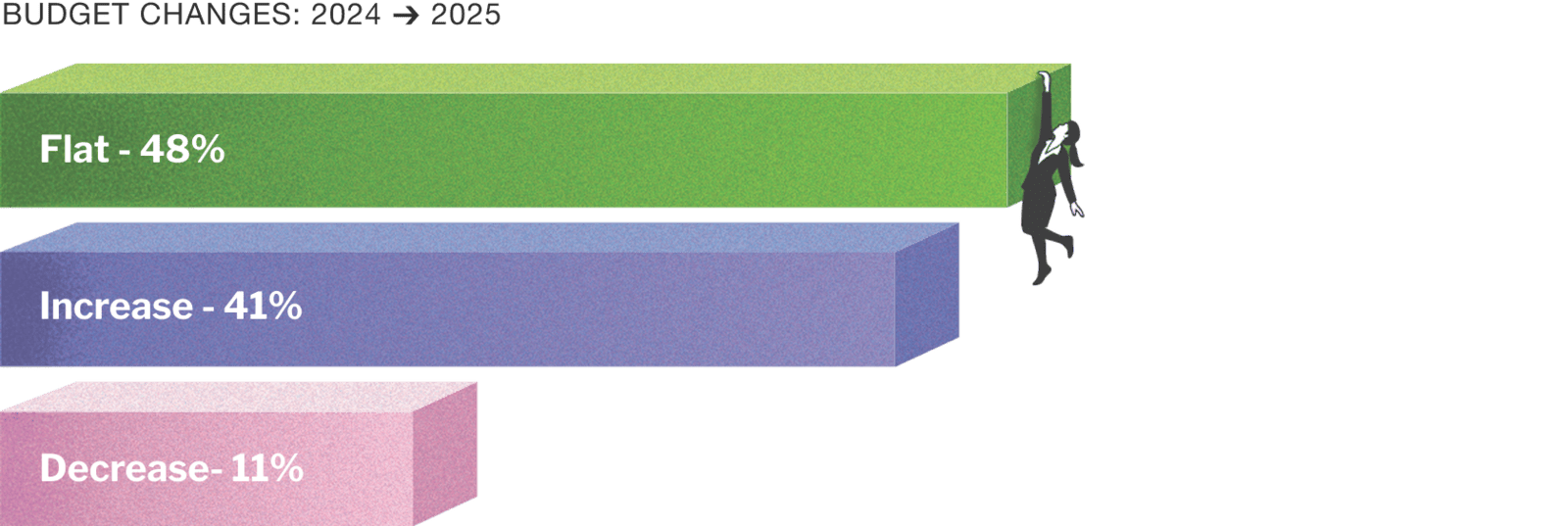

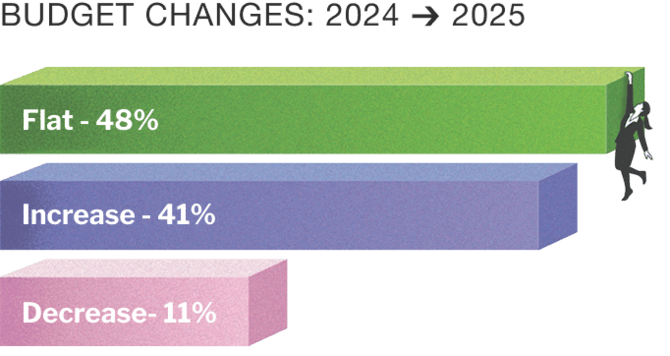

1. Budget stability with pockets of growth

Despite global economic headwinds, most APAC B2B marketers expect budget stability or modest growth in

2025.

Most marketers expect budgets to hold steady or modestly grow in 2025

For those lucky enough to receive budget increases, they grew by 14% on average. For those who had

decreased

budgets, the dropped by an average of 23%.

However, only 37% believe their 2025 budget will be sufficient to meet performance goals - leaving 63%

either

unsure or pessimistic.

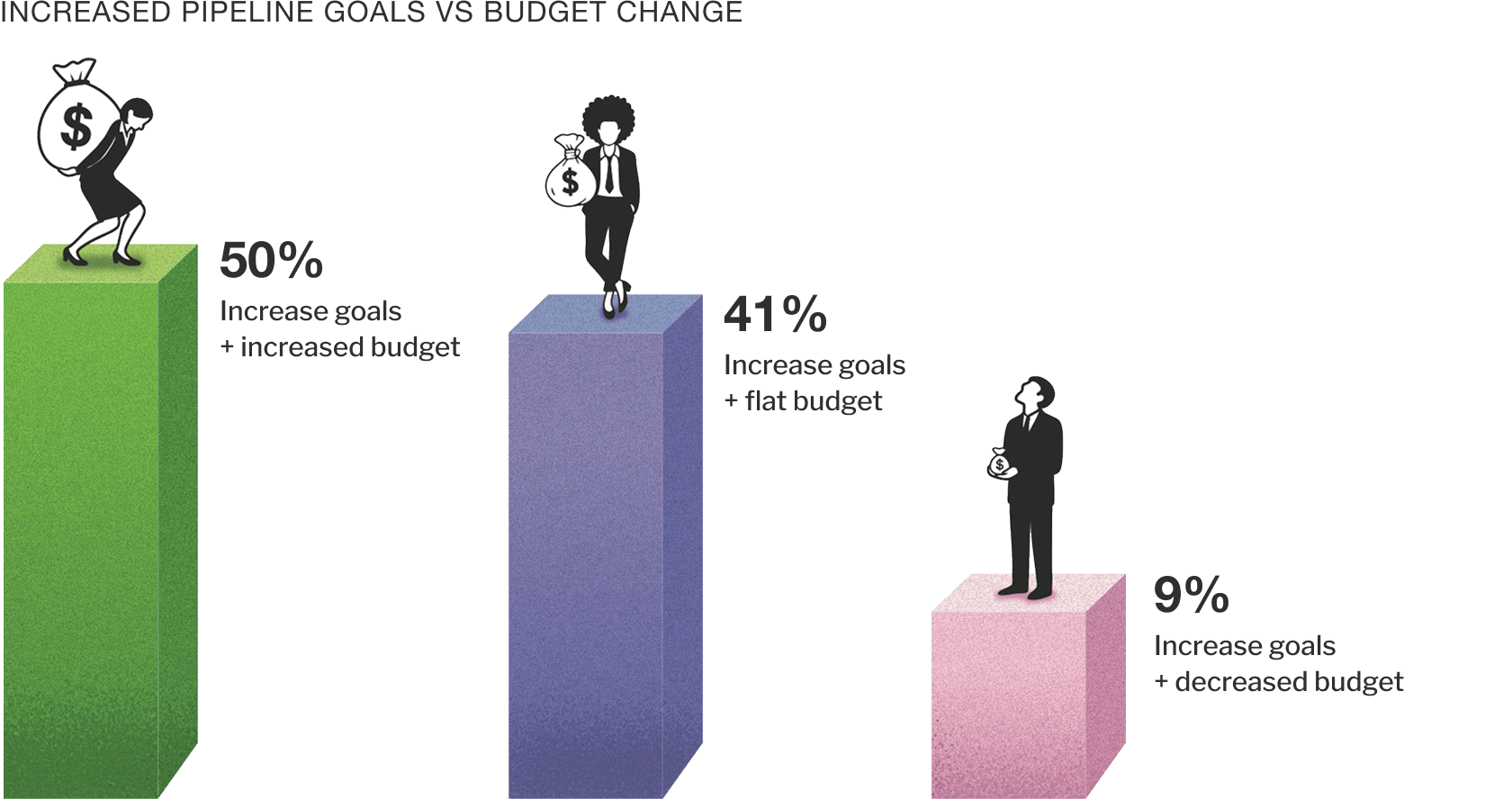

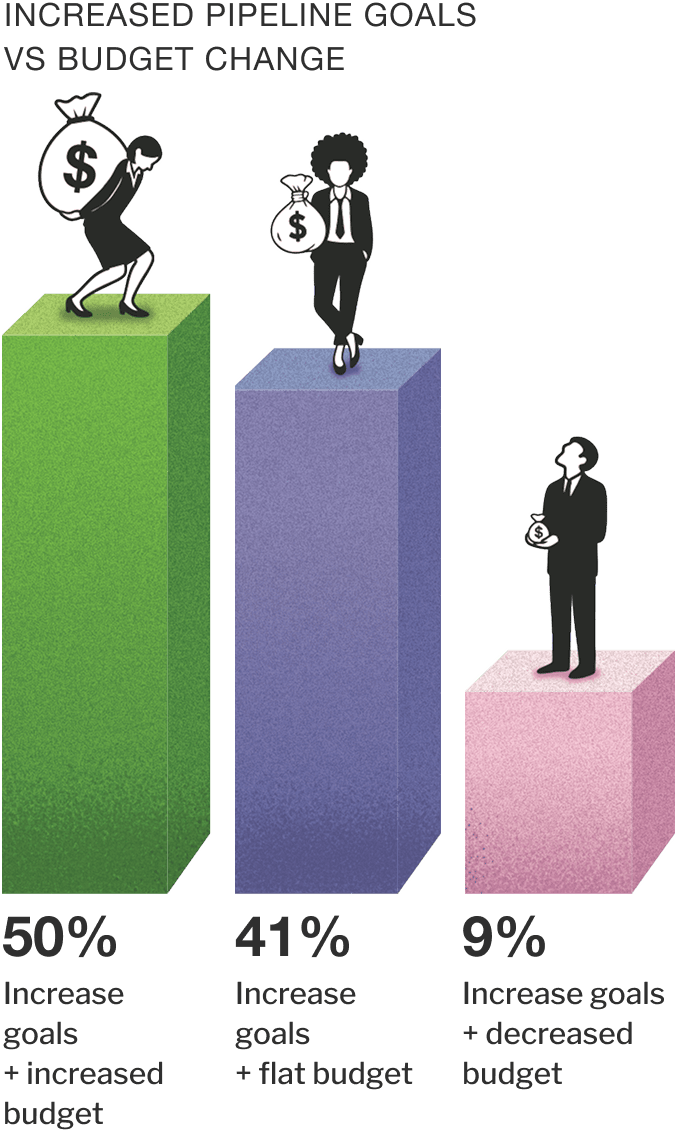

2. Revenue goals vs budget reality

Many marketers are chasing bigger pipeline goals without budget growth

Takeaway:

Nearly half of B2B marketers are being asked to deliver more with the same or fewer resources.

Efficiency,

automation, and precision targeting will be critical.

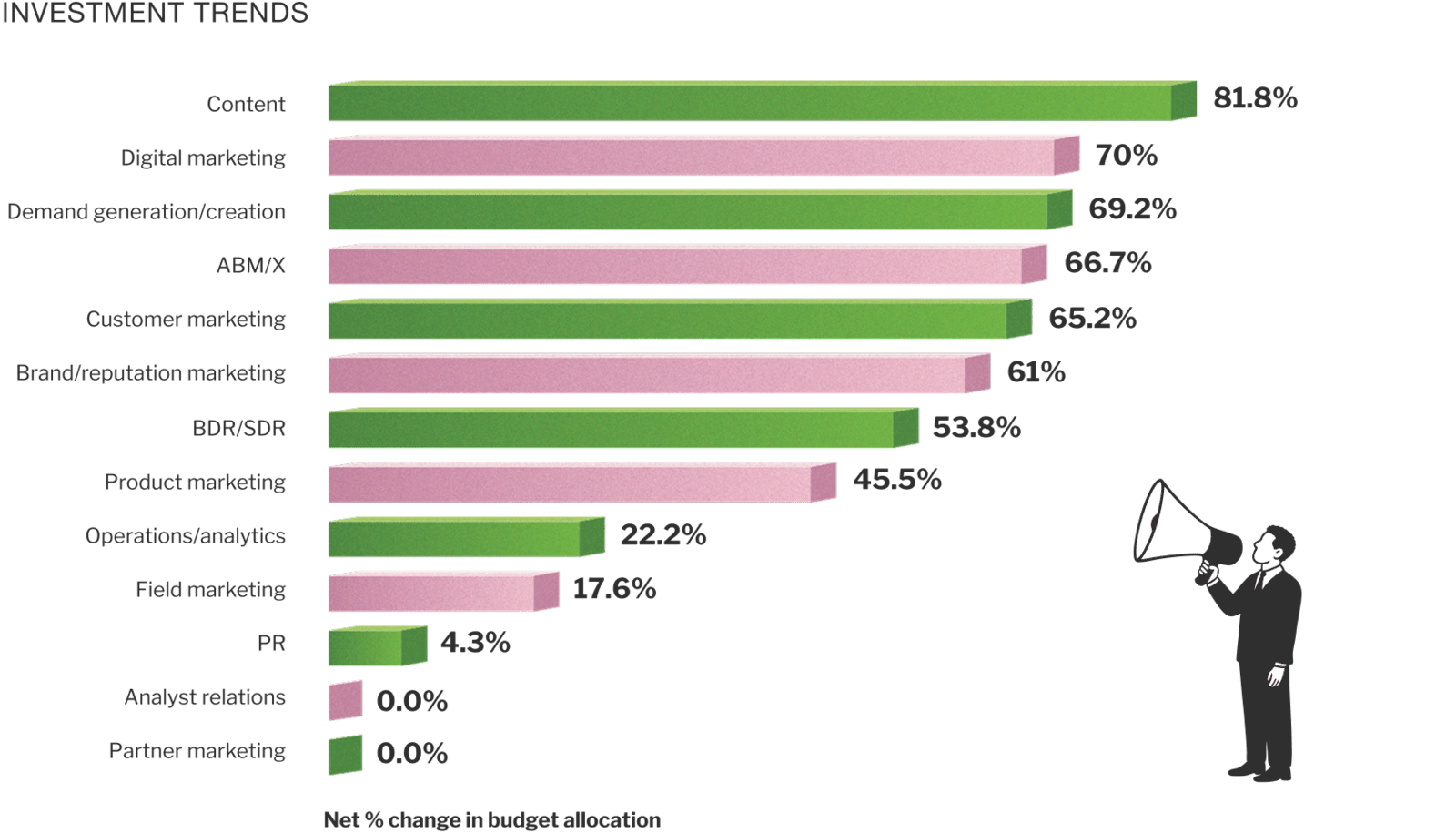

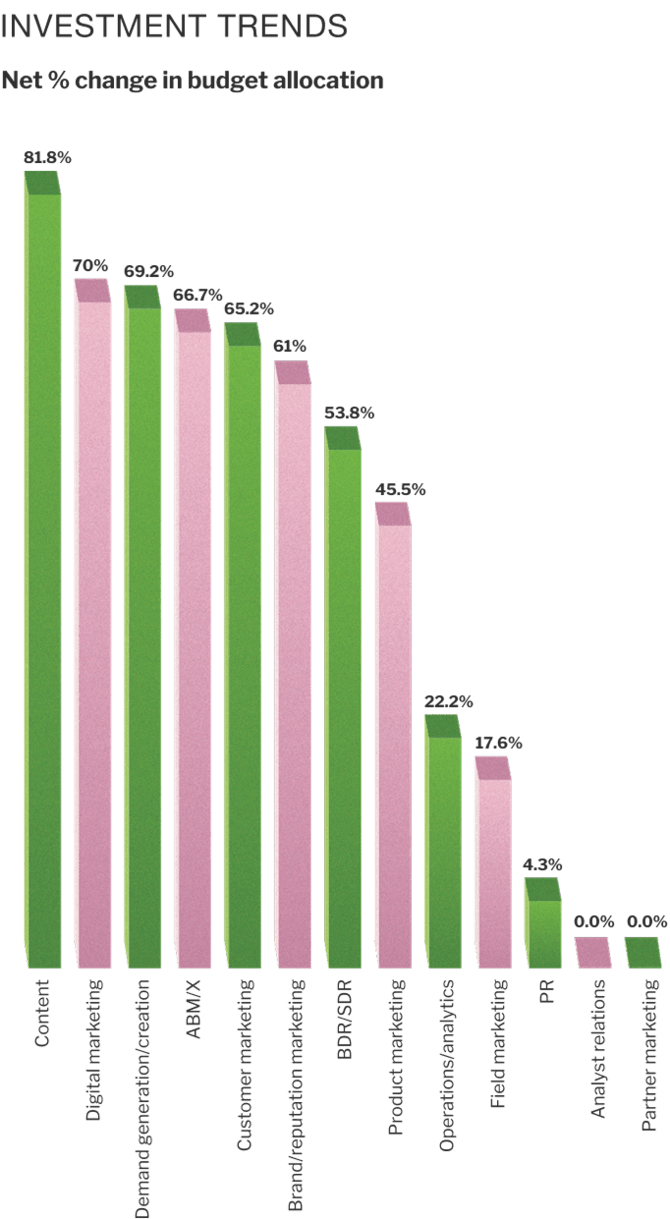

3. Investment trends by marketing activity

We asked marketers how they plan to distribute their budget during 2025. Activities seeing the highest

net

increase in investment (total respondents increasing less total respondents decreasing) include:

Content marketing

Content marketing

Digital marketing

Digital marketing

Demand generation/creation

Demand generation/creation

ABM/X

ABM/X

Brand

Brand

Customer marketing

Customer marketing

Despite nearly half of APAC marketers operating with flat overall budgets, the vast majority are

shifting

investment toward performance-driven areas (e.g., demand generation). Interestingly, those who received

budget

increases are also choosing to invest in these same areas.

Marketers are actively changing their channel/activity mix

Takeaway:

Marketers, regardless of whether they received a budget increase or not, are doubling down on what

drives

performance and revenue.

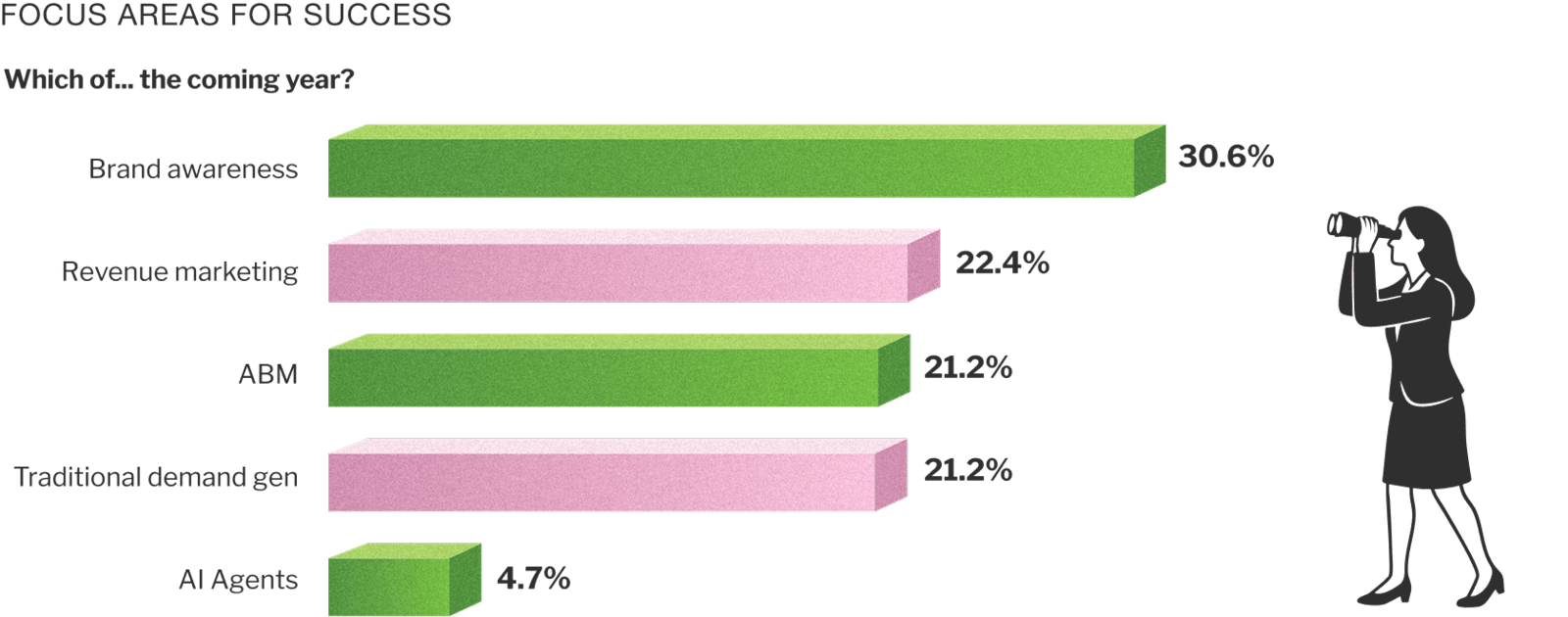

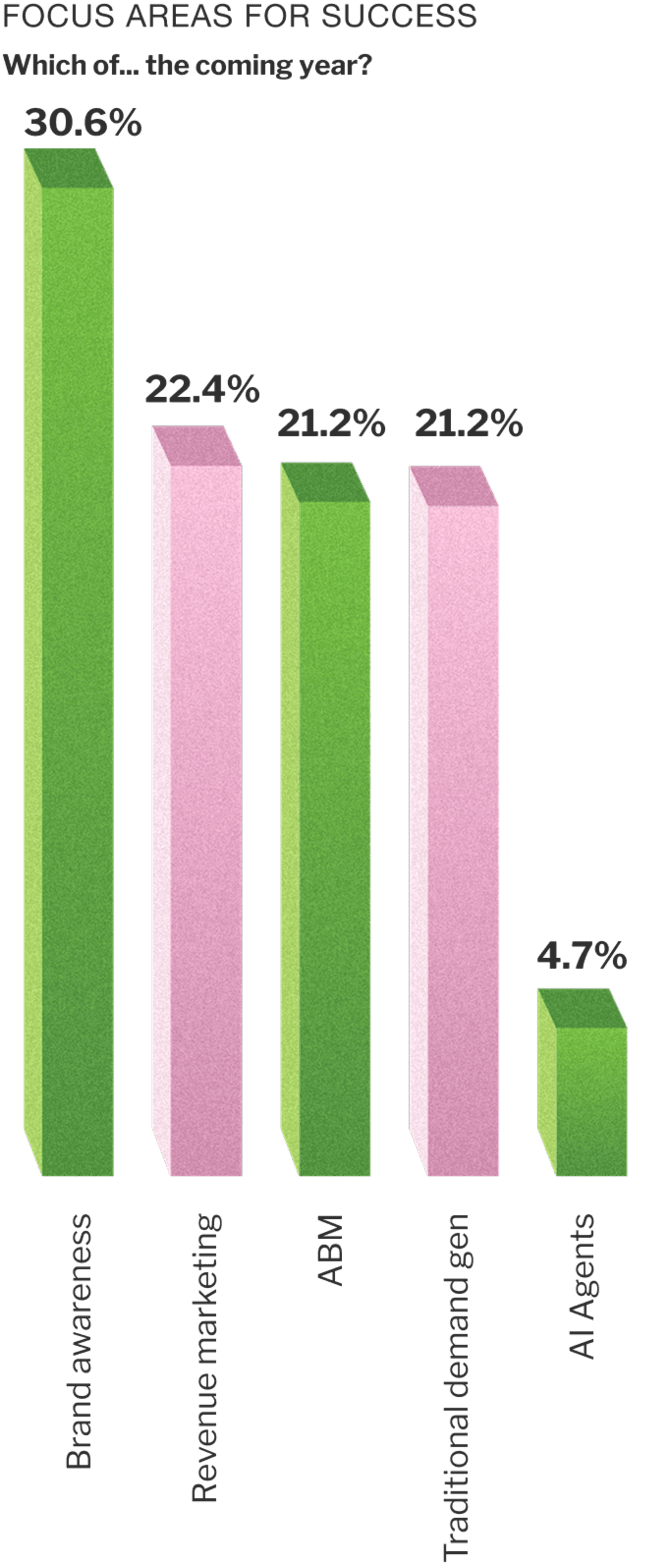

4. Brand vs demand: is the balance right?

So here lies the disconnect - despite budgets being channelled towards demand generation and revenue

marketing:

Marketers rank brand as #1 in terms of importance.

But actions speak louder than words. Consider the below:

50%

spend more on demand than brand.

Brand awareness ranks as the most important focus for success in APAC

Takeaway:

Even though brand is acknowledged by marketers as the top priority, marketers are prioritising

performance-led

activities, at the cost of long-term growth.

5. ABM adoption: room for growth

More than half of APAC marketers have adopted ABM but significant room for growth remains. While ABM has

crossed

into mainstream awareness, many marketers are still in early-stage adoption or trying to scale.

Reallocation trends suggest some marketers are using budgets to build ABM capabilities incrementally

rather

than securing additive funding:

55%

of APAC marketers report having a formal ABM program (vs. 77% in the US).

45%

remain without ABM in place.

Budget reallocation

not expansion - is funding most ABM development.

Takeaway:

APAC marketers are trailing US counterparts in ABM. Against the backdrop of increased pipeline

pressures, ABM

programs are an effective, efficient way to target and progress high-value accounts.

Part B

AI in the budget mix

Is confidence in AI all talk, little action?

1. State of AI budgeting

AI is starting to feature in APAC marketing strategies - but actual investment is lagging behind

confidence and

intent.

Only 29% of APAC marketers have a dedicated budget for AI in 2025 - well below the

52% reported in the US. Among those investing:

50

%

are using net-new funds

50

%

are reallocating from existing budget

This signals that while AI is on the radar and being employed in some fashion, it’s not yet seen as business-critical – more experimental than foundational. But with 59% of marketers operating with flat or less budget, and 63% lacking confidence in achieving their goals, AI could (and should) be a lever for efficiency, not just testing.

Early AI investments are spread across functions

Takeaway:

APAC marketers need to bridge the gap between AI confidence and investment into AI and have a clear

roadmap for

its use cases. Move from experimentation to deployment.

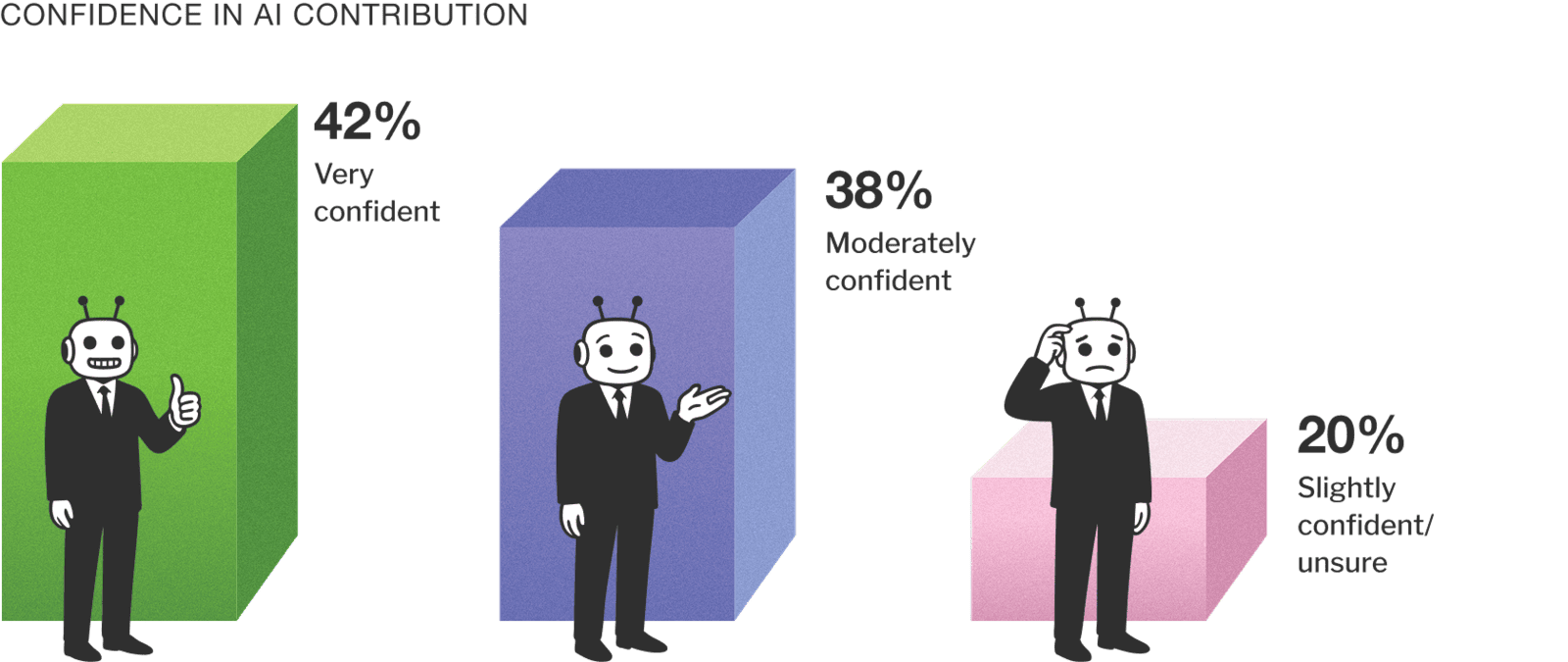

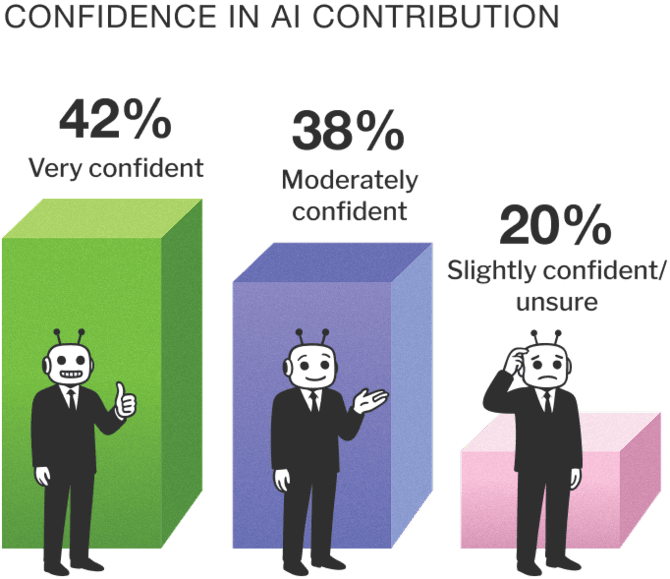

2. Confidence in AI contribution

Despite limited budget allocation, belief in AI's value is growing quickly.

80

%

of APAC marketers express confidence (moderate to very) in AI's ability to help achieve

marketing goals.

42

%

are very confident AI will help hit marketing goals.

Marketers growing more confident in AI helping achieve goals

Takeaway:

On the surface, confidence in AI seems strong. However, only 29% have a dedicated budget for AI. There

is a

disconnect - if most marketers believe AI will move the needle, why aren't they backing it with budget?

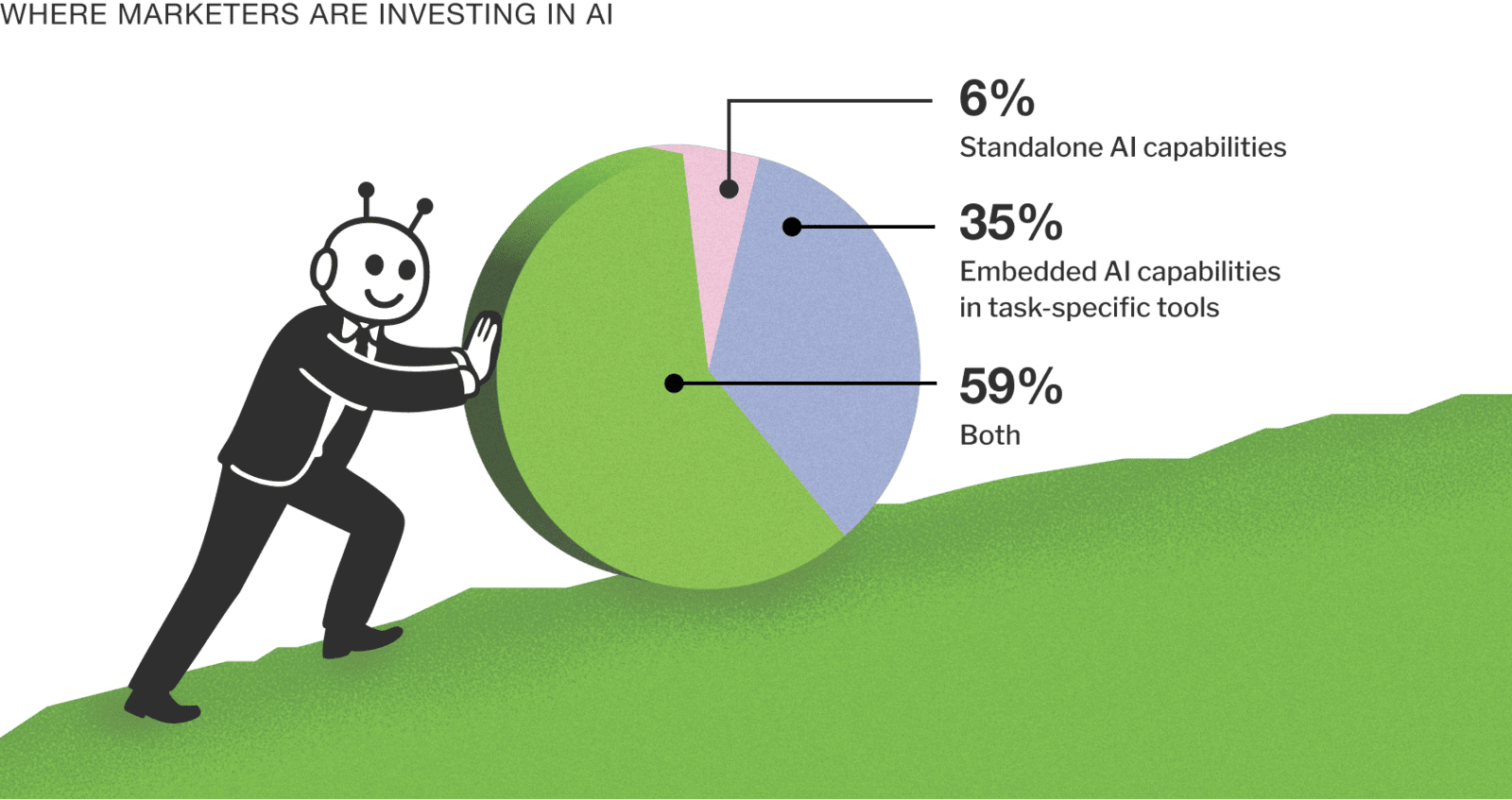

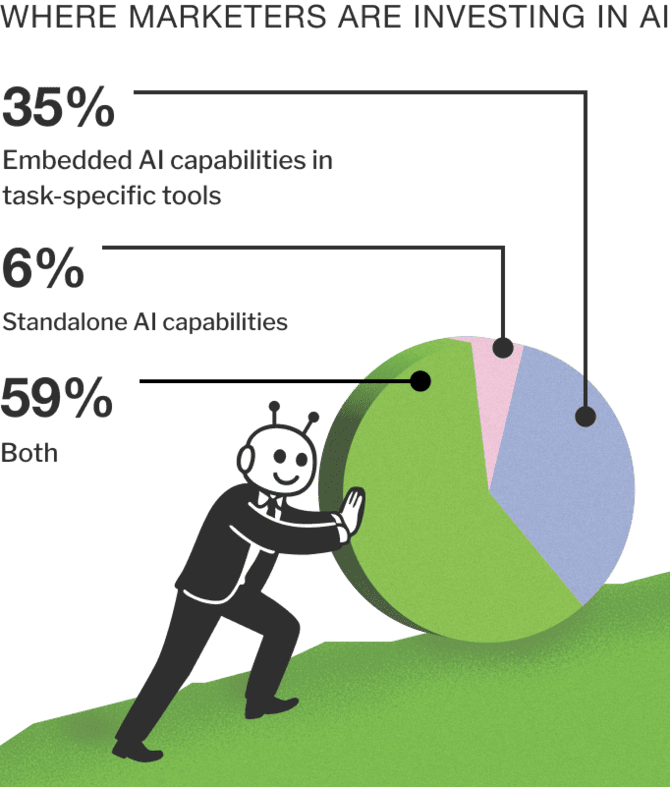

3. Martech selection and embedded AI

Even in the absence of dedicated AI budgets, buyers are shifting their evaluation criteria to favour

platforms

with embedded AI capabilities.

This is a pragmatic move. AI isn't just about deploying new tools, it can also be upgrading what you

already

use. Some marketing teams are acquiring AI by stealth: through CRM upgrades, content platforms, campaign

tools

and analytics engines that now come AI-enhanced by default.

Marketers favour embedded AI alongside standalone tools

Takeaway:

Vendors are AI-ing everything. That doesn't mean buyers are adopting strategically. APAC marketers need

to be

more deliberate. Ask not just “does this tool have AI?” but “how does this help me reduce cost, improve

performance, or move faster?”

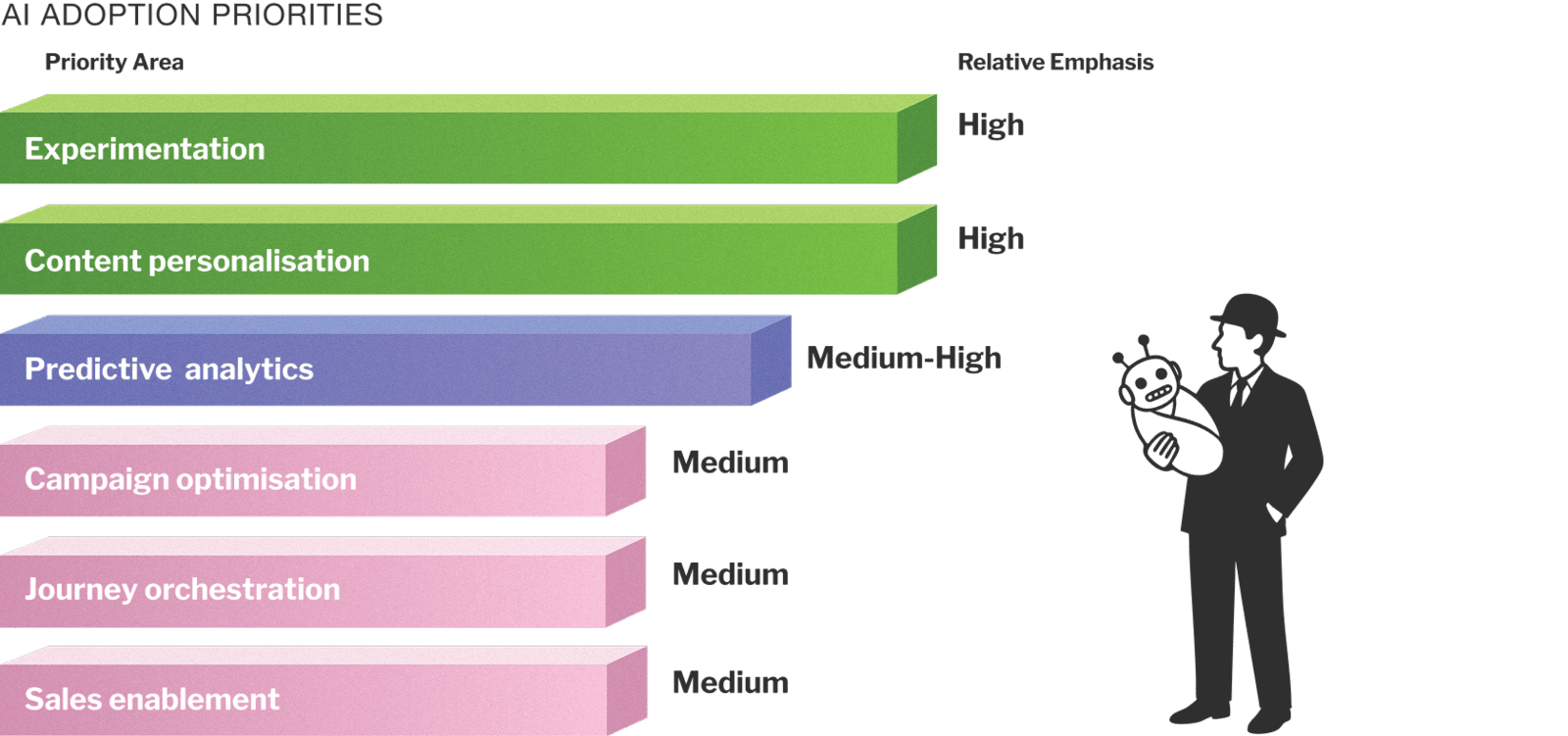

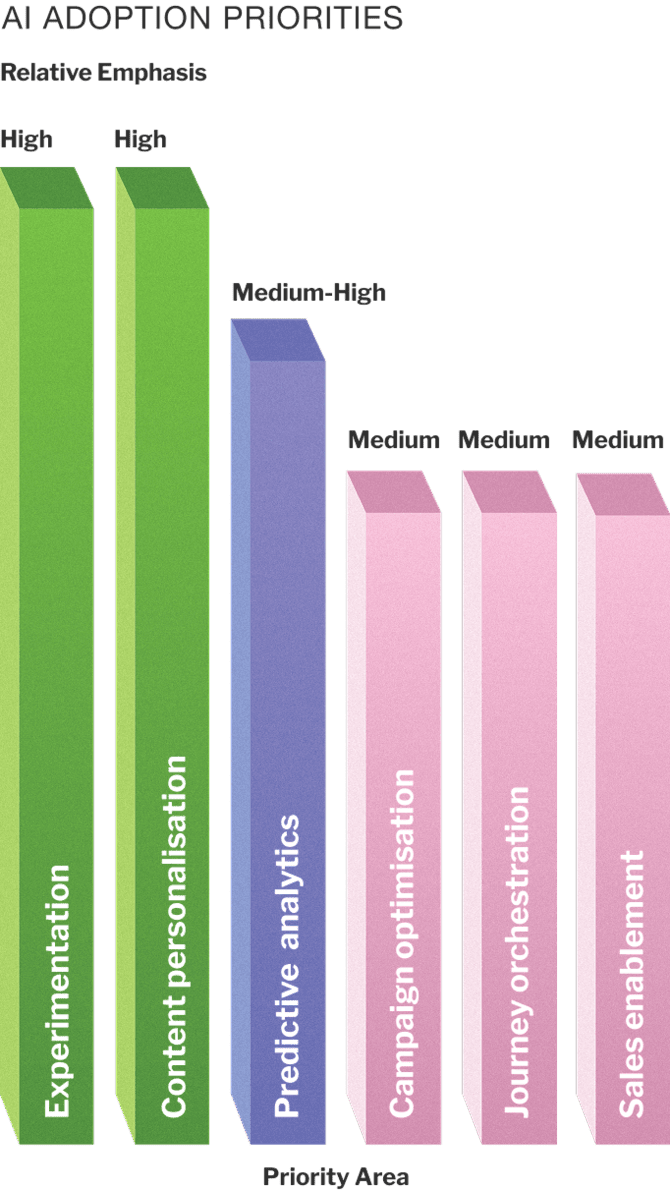

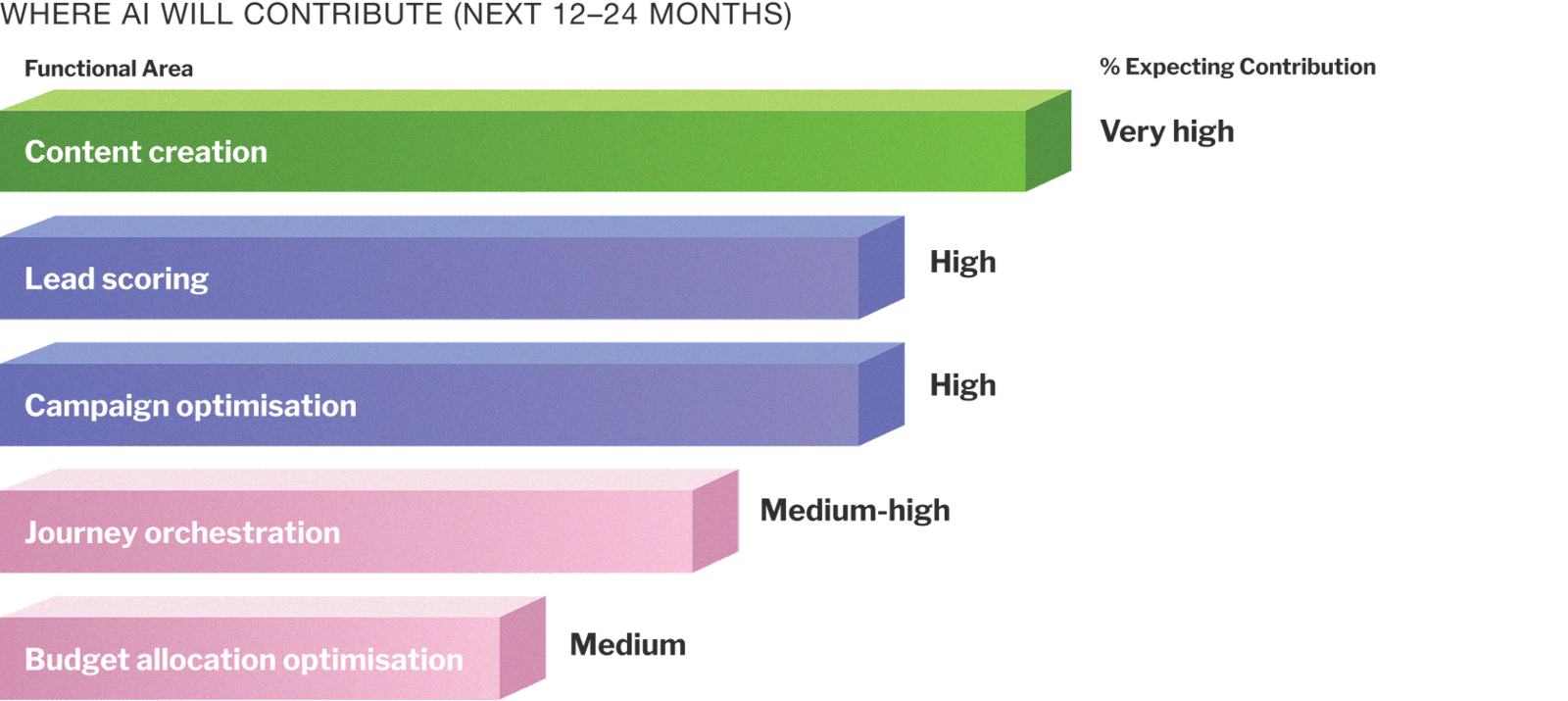

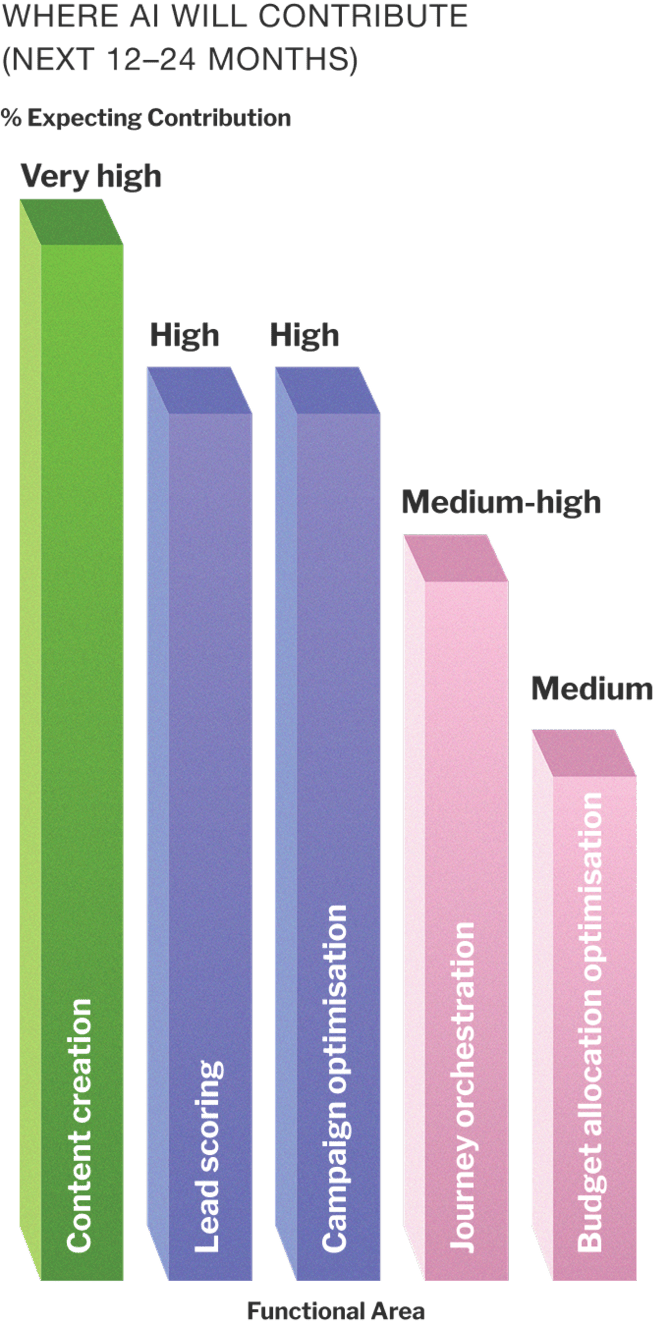

4. Expected AI impact (12-24 months)

Marketers see AI touching every major function in the near term, particularly:

Content creation

Content creation

Campaign optimisation

Campaign optimisation

Journey orchestration

Journey orchestration

Budget allocation decisions

Budget allocation decisions

Lead scoring and predictive analytics

Lead scoring and predictive analytics

Are marketers building the operational frameworks to support that impact? Strategy, training, and

governance

need to be implemented alongside aspiration and implementation.

AI expected to touch every major marketing function

Takeaway:

Marketers need to have a clear view about operationalising AI alongside culture, people and data

readiness to

activate them. If AI is going to span the full funnel, then training, experimentation, documentation and

accountability need to follow. The end goal would be to quickly operationalise AI across functions after

isolated pilots.

Part C

Actionable moves for B2B marketers

Turn words into action. Make your move today.

APAC marketers are caught in a tightening squeeze - rising pipeline goals, constrained resources, and

technological disruption. But amidst the pressure, there is opportunity.

Based on the findings, here are 8 key actions B2B marketers should consider in 2025 into 2026:

1

Reallocate budgets strategically

Don't wait for new budget - most marketers won't get one. Instead, reassign existing spend

to deliver

early and sustained pipeline: content marketing and demand generation shouldn't stop. But

also start

mapping out for longer-term projects such as ABM that will deliver consistent pipeline

aligned to the way

B2B buyers buy.

2

Prioritise brand for long-term pipeline

Brand is ranked as the #1 success driver - yet demand still dominates spend. In a buying

journey where 82%

of buyers choose the first vendor they contact, brand is how you become the first call.

Integrate

brand-building into revenue marketing frameworks. This could be apportioning budget into

your activities

for brand - and setting up ways to track and measure that impact.

3

Brand still needs local relevance

In APAC, brand is often managed globally - but buyer priorities are regional and local.

Marketers must

push for localisation of brand messaging and assets to reflect local economic climates,

buyer needs, and

language nuance, etc.

4

Tracking and measuring brand investment

An age-old problem is attributing ROI to brand investment. Why invest in brand when you need

to run

demand-gen activities to fill your pipeline? Marketers can solve the attribution issue

several ways. For

example, correlating share of search and uplift in intent against brand activity, using

tools that can

accurately measure buyer engagement, and building an attribution model that accurately

connects engagement

with marketing pipeline and revenue.

5

ABM is a competitive driver

With 45% of APAC marketers not running ABM, those who do are gaining a clear advantage -

because ABM

aligns directly with how modern B2B buying happens. ABM focuses on priority target accounts

and on

influencing entire buying groups. It also blends brand and demand, supports account-level

precision, and

builds alignment between marketing and sales.

6

Pilot AI where the impact is clear … and move quickly.

AI innovation is moving at a pace where marketers will not be able to “wait and see” before committing. Given that 59% of marketers have flat or less budget, AI can be where you find efficiencies and competitive advantage. Focus AI usage on content personalisation, lead scoring, and campaign optimisation – where ROI is most immediate. Treat AI like a growth driver, not a side project. Move as quickly as AI is innovating and evolving.

7

Embed AI into technology and vendor decisions

Favour martech vendors that include robust AI capabilities - it's a cost-effective way to

adopt AI without

new line items. Also, work with partners (e.g., consultants, agencies) that have AI as part

of their stack

and strategic approach.

Generative Engine Optimisation (GEO) is the practice of optimising content for AI-driven

search engines

like ChatGPT. As more B2B decision-makers rely on LLMs to inform their buying shortlists and

decision-making, GEO-optimised, structured content becomes crucial. Your brand must show up

- not just in

search, but also where buyers are now looking - popular LLMs such as ChatGPT, Gemini,

Claude, Perplexity

etc.

2025 will test the resilience and resourcefulness of B2B marketing leaders across APAC.

While budgets remain tight or flat for many, expectations for revenue contribution continue to rise -

forcing

marketers to make smarter, faster, and more focused investment decisions.

In this context, the most successful marketing teams in 2025 going into 2026 won't be the ones with the

biggest

budgets - but those that can balance short-term results with long-term growth, reallocate decisively

into

programs that can provide competitive advantage (e.g., ABM), and operationalise innovation (including

AI)

without waiting for perfect conditions.

Part D

Research methodology

Who, what and how we did it.

This research study was conducted by Green Hat, APAC's leading B2B marketing consulting and research

firm, in conjunction with 6sense Research.

A total of 155 senior B2B marketing professionals responded via on online quantitative survey during April-May 2025.

The US data was based on a 6sense study with 392 B2B marketers in the late months of 2024.

Roles represented

- CMOs, Marketing Directors, Heads of Demand Generation, Brand Managers, Marketing Operations Leads,

and

others

Primary industries covered

- Technology, Financial Services, Professional Services, Manufacturing, SaaS/Cloud

Company size

- Small (under 200 employees): 23%

- Mid (200-1000 employees): 42%

- Large (1000+ employees): 35%

Geography

- Companies primarily headquartered across Australia, Singapore, India, Japan, and broader APAC